Green, Social and Sustainability Bonds Q&A Part One: Digging into details on green bonds

Sustainable bonds (the collective term for green, social and sustainability bonds) is a growing asset class that has become a by-word for impact investing in a fixed income portfolio. As interest in this asset class continues to increase, so does the need for understanding the nuances behind them.

Here we share a few of the questions we are being asked about green bonds:

1. Do green bonds do more than just combat carbon emissions?

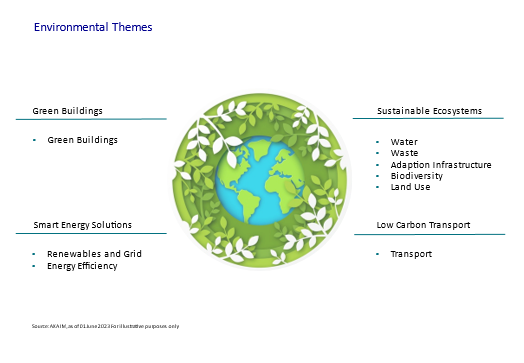

It could be assumed that green bonds are just a tool to help corporates and governments achieve their net zero carbon emissions targets. However, green bonds are used for a much broader range of environmental challenges. We see the global green bonds universe as being divided into four main themes: smart buildings, low carbon transport, sustainable ecosystems and smart energy infrastructure.

None of these themes work in silo and all can have a role towards lowering carbon emissions but, as the themes demonstrate, green bonds should be seen as part of the route to a sustainable economy beyond carbon emissions. Looking at the sub-themes within sustainable ecosystems demonstrates these separate priorities as well as the link to our carbon footprint:

Water

Water quality and quantity is a universal concern and one that impacts all individuals regardless of where they are living. Water stress – the combination of quality, quantity and access – is a focus for United Nations Sustainable Development Goals and one that companies from at-risk sectors such as agriculture to textiles can do more to address. While water stress may not be directly linked to a low carbon economy, the excessive use of it in some sectors and unchecked pollution controversies has an impact on the ecosystem and, therefore, how successfully carbon can be neutralised.

Waste

From food to electronics, the world’s growing population is putting pressure on natural resources by increasing demand for aspects such as energy, food and water. E-waste, for example, is one of the fastest growing waste streams in the EU and less than 40% is currently recycled

2. How do green bonds provide a positive impact for biodiversity?

Biodiversity loss is being addressed through green bonds. While still a new conversation, the Kunming-Montreal Global Biodiversity Framework (GBF) agreed in December 2022 during COP 15 has helped highlight the urgent need to protect nature. As companies realise the negative impact that biodiversity loss can have on their operations, green bonds are one solution for achieving a more nature-positive outcome. For example, we can think of New Zealand’s green bonds that are intended to advance the country's progress towards low carbon development, concretized in their recently reinforced Nationally Determined Contributions (NDCs), as well as the preservation of biodiversity: in 2020 the government published a biodiversity strategy setting a 30-year strategic direction which is supported by 5-year implementation plans, the last of which was released in April 2022. More specifically, it focuses on:

Living and Natural Resources and Land Use: sustainable agriculture, forestry, land restoration and nature-based solutions. This is of particular relevance as livestock farming accounts for c. 50% of gross greenhouse gas emissions

Terrestrial and Aquatic Biodiversity: protection of freshwater ecosystems, restoration of the natural environment including indigenous flora, and protection of marine species.

Investors are also increasingly aware of the need to engage with companies on the topic of biodiversity as the potential risks to their portfolios becomes more apparent. The GBF’s targets help with this conversation by providing guidance on a direction of travel for countries and companies. It is likely that companies will need to disclose more with regards to their biodiversity footprint especially as corporates embrace the GBF’s target of standardising accounting and reporting.

However, the lack of good quality data is a stumbling block: it tends to be location specific, difficult to compare and takes time for the research to come through and provide useful data. Nevertheless, with more regulation, we have seen a catalyst for positive development in data provision.

3. How to navigate volatile markets with green bonds?

While green bonds often only sit in a responsible investing bucket for investors, they may also offer investors a broader allocation option beyond impact. Most green bonds are either government or corporate investment grade and issued widely in developed market, as well as certain emerging market countries. This potentially positions the portfolio well as an alternative, or compliment, to a global aggregate allocation.

Just like other fixed income asset classes, green bonds can be invested into in different investment styles. At a time of volatility, having flexibility to manage duration and move across credit quality and geographies may be helpful to seek the best opportunities. Green bonds are now able to offer investors this flexibility in approach. While a dynamic approach that invests in high yield and emerging markets may only be for investors with a higher risk appetite, the ability to invest across the duration curve may also be a useful tool for investors looking to reduce interest rate risk through short duration bonds. This means that investors may keep the benefit of green bonds while reducing their duration profile without necessarily giving up yield due to the characteristic of the universe and current yield curve inversion.

The growth of green bonds issuance allows investors greater scope for how they allocate to the asset class whether as an alternative, or a compliment, to a global aggregate or reflecting different styles and risk profiles within their portfolios.

References to companies and sector are for illustrative purposes only and should not be viewed as investment recommendations.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.