Adding to the toolkit: inflation-linked bonds

When looking to mitigate against the effects of inflation, inflation-linked bonds can be an important tool in an investor’s kitbag. Knowing how they work and what they can do is, therefore, important.

Inflation-linked bonds help against inflation risk because they link a bond’s principal value (the amount to be paid at the end of the bond’s life) to the price index such as CPI that reflects the rate of inflation. As a result, inflation-linked bonds are more than a coupon strategy as indexation to inflation is impacting the bond’s principal that as a result grows over time.

If inflation is 2%, the principal value of an inflation-linked bond will increase by 2% each year until the bond matures. This process is known as inflation indexation.

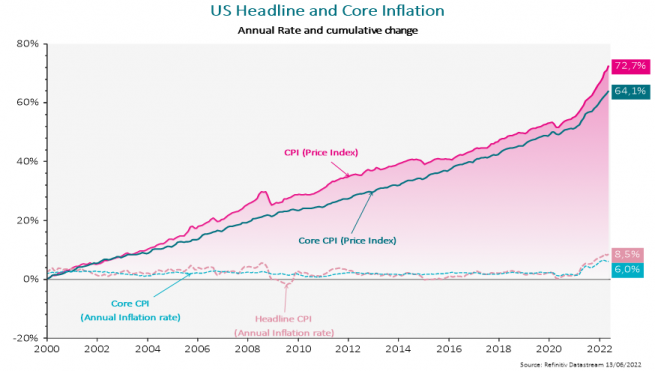

In practice, if an investor had bought an US inflation linked bond in 2000 and held it until today

Alongside this, as coupons are paid based on a percentage amount of the principal, the coupon payments will also increase. This is how inflation-linked bonds can help investors mitigate the impact of inflation on their portfolios and protect the real value of their assets

Providing a real yield for investors

On top of this, as inflation indexation is guaranteed by the issuer, inflation-linked bonds also provide investors with a real yield. Real yields represent the premium that investors can lock-in on top of realized inflation.

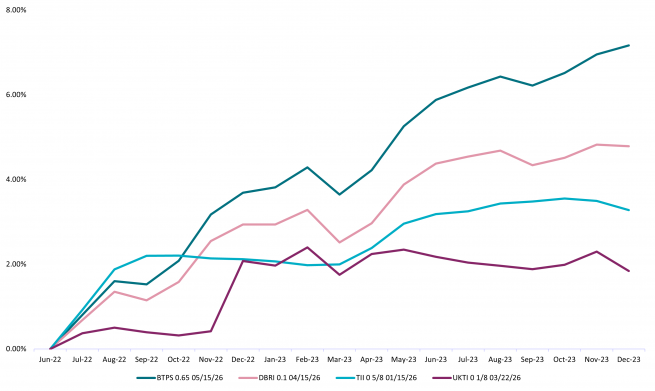

The real yield added to the inflation indexation forecast will give the equivalent to a running yield that could be compared to the yield of a nominal bond. This calculation is known as the total income of an inflation linked bond.

As this chart shows, in most cases inflation is published monthly so the income is not a straight line and would differ from one month to another. This also demonstrates that high inflation should mean high income for inflation-linked bonds.

Inflation-linked bonds can offer investors an income that is adjusted to reflect inflation and so may help reduce the erosion inflation can cause to their portfolio value. As well as understanding the methods used to calculate an inflation-linked bond’s value, there are other elements to consider when deciding how to invest in these bonds. In the next in the AXA IM Inflation Series, we will look at duration and how this impacts inflation-linked bonds.

Inflation

Inflation can erode the real returns of investments however tools like inflation-linked bonds could help investors mitigate the effects of inflation on their portfolio.

Find out more

Watch the other modules from our inflation series

The objective of this series is to make inflation-linked bonds investing simple to investors.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.