Prospects for US Treasuries: Avenues for Investors through ETFs

KEY POINTS

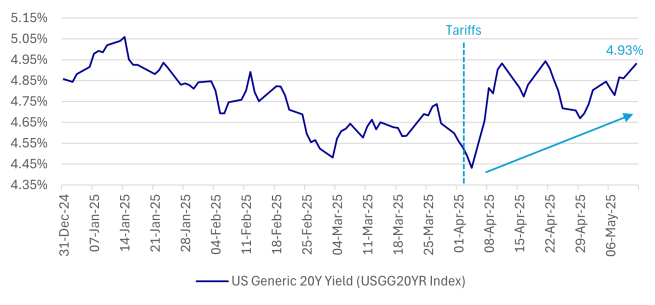

In recent weeks, US Treasury yields have experienced notable fluctuations, particularly following President Trump's announcement of a stricter global tariff policy. After hitting a low in early April, the 20-year yield surged, raising concerns about future trends amid ongoing policy uncertainty and deleveraging. Typically, during periods of stock market stress, investors seek the safety of US Treasuries, which drives yields down and pushes prices up. However, this time, the opposite occurred. Notably, the US Generic 20Y yield rose to 4.93% on 12 May 2025, compared to 4.56% the day before the announcement

However, US Treasury returns have remained relatively stable and positive; the ICE US Treasury index recorded a total return of 1.92% year-to-date1. Fears of a mass exit from Treasury holdings have not materialised, as the depreciation of the dollar has outweighed the rise in bond yields, favouring other major currencies and suggesting capital repatriation to creditor nations. With significant tariff levels increasing the risk of a US recession, business and consumer confidence indicators have sharply declined, potentially exerting further downward pressure on the dollar.

High treasury yields: implications and opportunities

Several interconnected factors are currently shaping Treasury yields. Increased market volatility has led many investors to liquidate assets, including Treasuries, to raise cash and meet rising margin requirements. This trend has intensified as traders seek to reduce their exposure to Treasury-related derivatives, contributing to upward pressure on yields. The recent spike in the VIX index and ongoing uncertainty reflect a broader strategy to manage risk during this challenging financial period.

Concerns about rising budget deficits also play a significant role in driving yields. As fears surrounding fiscal imbalances grow, the necessity for increased Treasury issuance becomes clear. Larger deficits necessitate more bond sales, resulting in an oversupply in the market that pushes prices down and yields higher. Ongoing discussions in Congress regarding potential tax cuts and new spending initiatives could further complicate the fiscal landscape, leading to additional upward pressure on interest rates.

Inflation concerns significantly influence investor sentiment as well. Heightened fears regarding inflation, particularly with the implementation of tariffs, have prompted a reassessment of the risks associated with Treasury securities. The notable increase in the two-year breakeven inflation rate reflects growing apprehension about short-term inflationary pressures. As investors navigate the implications of tariffs on pricing and economic stability, these inflation concerns are likely to continue impacting Treasury yields moving forward.

If the scenario of "higher-for-longer" yields materialises, it may present an opportunity for investors in US Treasuries. With yields remaining elevated, investors can benefit from enhanced carry on their investments, providing a more enduring return profile. As they navigate the implications of tariffs on pricing and economic stability, these factors render US Treasuries an attractive option for those seeking stable and reliable returns.

Rationale for investing in US Treasuries

Recent fluctuations in the Treasury market underscore its vital role in setting global risk pricing and facilitating hedging, funding, and leveraged investments. Despite headwinds in the US economy, there are five compelling reasons for investors to consider including US Treasuries in their portfolios.

Low default risk – Treasuries continue to offer low default risk, bolstered by the fundamental resilience of the US economy and its structural importance in the global financial tissue. This stability instills confidence in the safety of investors' allocations.

High carry – The current environment features elevated yields, which are higher than in previous years. This not only enhances expected total returns but also positions Treasuries as an attractive option for income-seeking investors, particularly in a climate where stable revenue streams are highly valued.

Downside risk priced in – Potential downside risks, such as inflation and the likelihood of sustained higher interest rates, appear to be factored into current yields. Recent yield charts suggest these concerns may be overstated, especially as some trade agreements begin to materialise, which could lead to lower yields. If the developed above scenario of "higher-for-longer" yields does not materialise, it could enhance both capital appreciation and carry.

Asset class correlation – The correlation between equities and Treasuries can vary based on the macroeconomic context and prevailing economic cycle. Thus, US Treasuries play a crucial role in multi-asset portfolios, particularly as hedges in disinflationary environments. Investors should remain cognisant of risks, especially those related to curve steepening, enabling them to select the maturity of Treasuries that best aligns with their market expectations and risk management strategies.

Robust liquidity – Liquidity in the Treasury market remains strong, as Treasuries are among the most liquid instruments available. This liquidity provides investors with "dry powder" to allocate to other investments, such as illiquid assets or credit, particularly while spreads remain relatively tight. The ease and low cost of selling Treasuries further enhance their appeal, especially for short-dated Treasury ETFs, which present minimal drawdown risk.

Investment opportunities with US Treasuries ETFs

Considering these dynamics, ETFs focused on US Treasuries present compelling opportunities for investors. These vehicles enhance diversification by providing access to a broad array of Treasury securities across various maturities. This structure allows investors to spread their risk rather than holding a single bond while benefiting from relatively high yields and effective risk management. Additionally, ETFs are highly liquid and typically feature low fees, making them attractive as cost-effective investment options.

Government bonds, particularly Treasuries, rank among the most widely traded and least risky assets in terms of default risk, making them essential for portfolio diversification—an effective strategy for managing risk in uncertain market conditions. With Treasury yields currently positioned above levels seen since the 2008 financial crisis, investors willing to hold these bonds to maturity should earn appealing yields with minimal default risk. This environment is particularly favourable for income-seeking investors looking to integrate Treasuries into their investment strategies.

Investors can also strategically utilise the duration and various maturities of US Treasury ETFs, whether short or long, to align with their investment objectives and risk tolerance. Given the current landscape, now may be an optimal time for investors to leverage the stability and reliability of these assets through ETF investments.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.