The interest rate threat

Equity markets continue to swing in reaction to US President Donald Trump’s latest social media post or interview - going one way if the news is of positive progress in negotiations (albeit denied by Iran), or the other when an escalation of the conflict seems imminent. The risk assets outlook remains unchanged insofar as further declines or a rebound from here depend on which path the war takes.

There has been a change in market dynamics, however. Oil-sensitive industries continue to move alongside the price of oil, but for the technology sector, the key factors have evolved.

Technology stocks are particularly sensitive to interest rates due to the long duration of their earnings relative to companies in other sectors. This link was starkly apparent in 2022 when economies reopened after Covid lockdowns. Inflation resurged and central bank policy rates rose in response. The 10-year US Treasury yield jumped from 1.6% to 4.2% while the Nasdaq fell by some 35% over the year.

This correlation weakened in February, however, as other factors began driving returns. Hardware technology companies saw their share prices rise thanks to big increases in artificial intelligence-related capital expenditure, while software stocks declined due to perceived threats to business models from artificial intelligence tools.

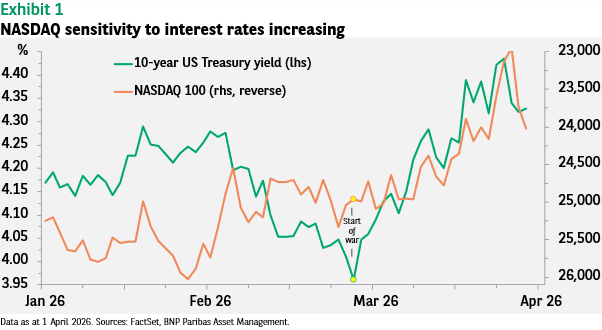

The outbreak of the Iran war led to the unwind of very long and short positions in these sectors (as well as in gold and bitcoin). This overwhelmed the impact from the large jump in Treasury yields after 27 February and the net change in the Nasdaq index was limited.

Now that positions have been reduced, interest rate sensitivity has returned. As Treasury yields have risen further, the index has fallen (see Exhibit 1). We have also seen the return of the positive correlation between hardware and software stocks, which had broken down earlier this year.

This new equity market dynamic suggests the outlook for tech stocks is arguably more positive than it is for other sectors. The risk is that if the war escalates and oil prices rise further, Treasury yields could continue to climb. But a significant jump in oil prices might instead lead markets to begin pricing in a recession, which would likely point to lower interest rates.

In this scenario, technology stocks could return to their “defensive” role within equities as demand is comparatively resilient and tech companies would likely continue their AI infrastructure investments.

If negotiations to end the conflict do succeed, lower interest rates would likely spur a market rally. In our view the Federal Reserve’s relatively patient tone about the impact of higher oil prices on inflation, in contrast to a more reactive European Central Bank, provides further support for US equities.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.