Take Two: Middle East conflict shakes markets; China cuts annual growth target

What do you need to know?

Global markets endured further volatility last week after the US and Israel took coordinated military action against Iran. Stocks fell sharply at the start of the week before then recovering some ground. Government bond yields rose also reflecting concerns over inflation, while oil prices increased on supply concerns. Over the week to Thursday’s close, the MSCI World NR Index fell 2% while the S&P 500 lost 1%, the Eurostoxx 600 fell 6% and Japan’s Nikkei fell 7%.* Market sentiment will likely remain largely driven by the scale and duration of the conflict.

*In US dollar terms. Source: FactSet, data as of 5 March 2026

Around the world

China cut its annual economic growth target to a range of 4.5%-5%, its lowest official goal since 1991, as it unveiled its new Five-Year Plan. The figure represents a decrease from its previous growth target of “around 5%”, which was met in 2025, as the country continues to face weak domestic consumption, property market challenges and global trade tensions. The draft Five-Year Plan, which will be put to a vote this week, also includes investments in innovation and technology, transport and energy, as well as further efforts to boost household spending.

Figure in focus: 1.9%

Eurozone annual inflation unexpectedly rose to 1.9% in February, the first time it has remained below the European Central Bank’s 2% target for two consecutive months since April 2021. The market had expected price increases to remain steady at 1.7%, to match January’s rate. Core inflation, excluding energy, food, alcohol and tobacco, increased to 2.4% from 2.2% in January. Separately, Eurozone GDP growth expanded by 0.2% in the fourth quarter, down from the previous estimate of 0.3% and Q3’s 0.3% growth. Elsewhere, the UK economy is now expected to expand by 1.1% this year, down from November’s prediction of 1.4%, according to new official forecasts.

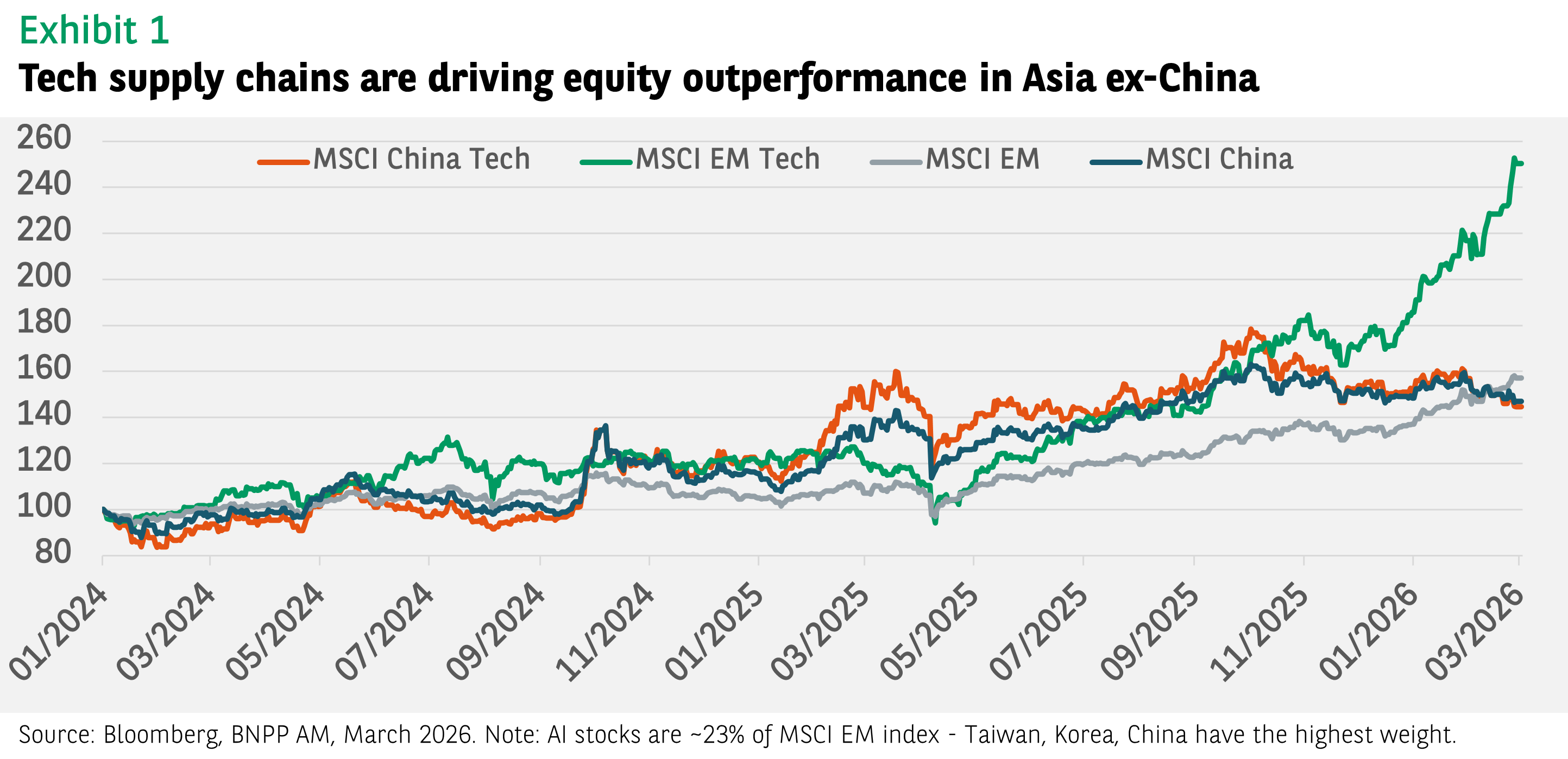

Chart of the week

The divergence between Asian markets, especially in the technology sector, highlights a dynamic shift in the regional landscape, driven by the global artificial intelligence capital expenditure boom. Hardware hubs in Asia-ex China, notably Taiwan and South Korea, are thriving due to increased demand for high-end semiconductors and advanced packaging. China’s tech sector, however, presents a more nuanced picture. While recent policy reforms and domestic AI innovations like DeepSeek have spurred some recovery, the sector still trails regional peers. China is actively working to establish its own technological leadership and independence, across software and hardware domains. Ongoing headwinds such as US export restrictions and regulatory uncertainty have kept investors on the sidelines.

Words of wisdom

EURO-3C: A €75m European Union project aiming to deliver “cutting-edge digital services” through telecommunication networks, cloud infrastructure and edge computing – which makes data processing faster. The European Commission unveiled the project, termed EURO-3C, at the Mobile World Congress last week. It said the initiative would reduce reliance on third-country providers, while bringing high-speed secure computing power closer to end-users. Involving a consortium of 87 companies and organisations, the project is intended to boost Europe’s digital and industrial competitiveness.

What’s coming up?

On Monday, China issues its latest inflation data while Tuesday sees a final estimate of Japan’s Q4 GDP growth published. The US reports February’s inflation rate on Wednesday - in January, US annual inflation fell to 2.4% from 2.7% in December. On Friday, Eurozone industrial production figures are published, while the UK posts monthly GDP data for January, and the US reports a second estimate of its Q4 GDP growth rate. The earlier estimate showed US GDP growth slowed to 1.4% in Q4 from Q3’s 4.4% growth.

Read more insights at the Investment Institute

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.