A decade since the Paris Agreement and the green bond market has never looked better

KEY POINTS

The green bond market’s momentum is showing no signs of slowing – it is becoming increasingly standardised, transparent and credible, which is in turn driving an ever-rising demand for the asset class.

The Paris Agreement - adopted by 196 parties in 2015 – which aimed to limit global temperature rises to well below 2°C above pre-industrial levels, but preferably much lower, has likely proved to be a tailwind for the sector.

China, the world’s second-largest economy, issued its first green sovereign bond in April in a bid to attract international capital to support its environmental ambitions. Listed on the London Stock Exchange, the yuan-denominated bond raised a significant RMB6bn (US$833m).

It is the sector’s latest significant development which has markedly expanded in recent years. In 2024, the green bond market enjoyed a record $447bn in issuance

What’s more, green bonds - the proceeds of which are earmarked for environmentally friendly projects - outperformed the conventional bond market in 2024 and have done so for six of the last eight years.

Growth goes beyond Europe

Europe continues to dominate the green bond market in terms of issuance – driven in part by the region’s commitment to sustainability. The European Commission is funding up to 30% of its post-pandemic economic recovery package, Next Generation EU, via green bonds - which would make it the largest issuer of such bonds in the world.

Meanwhile, Germany’s fiscal plans could also prove to be beneficial for the green bond market. The world’s third-largest economy recently approved a €500bn infrastructure and defence spending package including €100bn pledged to climate and energy transition projects, aimed at reducing carbon emissions and building sustainable infrastructure

Looking beyond Europe, sovereign green bond issuance in Asia and emerging markets is also increasingly under the spotlight and certainly, Beijing’s recent move into the universe has created a new opportunity for investors in a market traditionally dominated by euro and dollar issuance.

We do expect to see lower green bond issuance in the US this year, given the backlash against environmental, social and governance issues which has recently been witnessed there, especially from the new US administration. Tellingly, the US has seen the slowest start to corporate green bond issuance in a decade, according to Bloomberg, though municipal green bond issuance is still strong.

Greater transparency and credibility

Green bond regulation is continuing to develop as the market evolves and grows. The new European Green Bond Standard, applied from December 2024, sets out best practice for issuers in the asset class.

It requires issuers to allocate at least 85% of a bond’s net proceeds to activities defined as ‘green’ under the EU Taxonomy.

A recent study from the Bank of International Settlements

A swathe of potential opportunities

The green bond is becoming increasingly mature and is increasingly diversified across region, sectors and issuers. It encompasses some highly liquid, typically defensive segments such as sovereign and quasi-sovereign debt, as well as those tending to yield more but that are still robust such as investment-grade corporate bonds, and riskier but potentially higher reward parts of the market like high yield and emerging market debt.

We are no longer seeing a ‘greenium’ – the premium price that green bonds have historically attracted compared to conventional bonds. As the market has expanded and diversified, the supply/demand imbalance has levelled out, and green bonds as an asset class are generally no more expensive than their conventional counterparts – while offering the opportunity for investors to make a positive impact.

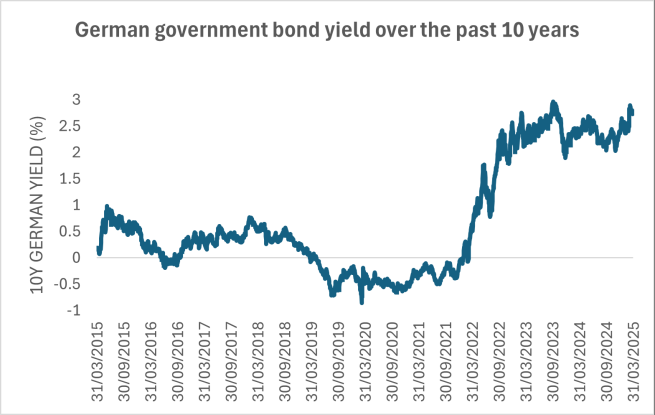

Yields soared in 2022 on the back of persistent inflationary pressures and have stayed since then at historical high levels despite central banks easing rates over the past year (see chart below). As such, we believe green bonds represent a potential opportunity for investors to gain exposure to an attractive bond market with access to the entire range of fixed income performance drivers.

At the same time, volatility has significantly increased over recent years, not least in the current highly uncertain environment, against a backdrop of trade wars, policy uncertainty and other geopolitical concerns.

This means investors must be agile to be able to seize opportunities in terms of asset allocation and geographical allocation as well as in duration management.

Uncertainty could weigh on risk appetite and potentially push credit spreads wider, especially since they currently stand at historically tight levels. For this reason, investors could potentially benefit from taking a diversified approach and could consider an allocation to green bonds given the asset class’s breadth and range.

A tool in the net zero transition

The green bond market has enjoyed strong growth and performance over the past decade and there are plenty of reasons to be optimistic about the future. There is a huge need for investment in the transition to a low-carbon economy, and green bonds are already an effective tool to support issuers in this effort.

Thanks to this structural support, as well as the asset class’s growth, liquidity and diversity, we believe green bonds are a potentially attractive way to gain exposure to the broader bond market through a diversified exposure that can potentially enhance return prospects when coupled with flexibility, while delivering a positive and measurable impact.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.