Euro credit sectors offer opportunities despite market volatility

KEY POINTS

Despite facing multiple episodes of volatility in recent years, the euro credit market has demonstrated notable resilience, consistently delivering solid returns to investors.

Today, Euro corporate bond markets continue to benefit from resilient fundamentals, attractive income levels, and sustained investor inflows. In the first quarter of 2025 alone, European fixed-income funds attracted over €83 billion in net inflows1, reflecting a cautious yet opportunistic investor mindset. With yields remaining elevated, we expect investor demand to grow further as many seek to lock in favourable returns.

However, not all issuers are created equal. We are witnessing increasing divergence across sectors and countries, driven by geopolitical tensions, regulatory shifts, and uneven macroeconomic conditions. For instance, credit standards have tightened in Germany while easing in Italy, reflecting regional imbalances. Moreover, sectors such as luxury goods and autos are more exposed to external demand shocks, while financials and utilities continue to benefit from conservative capital strategies.

In this environment, issuer selection remains critical. Identifying companies with strong fundamentals, prudent financial management, and sectoral resilience is key to capturing long-term value in euro credit markets.

- Source: Morningstar, as of 31 March 2025

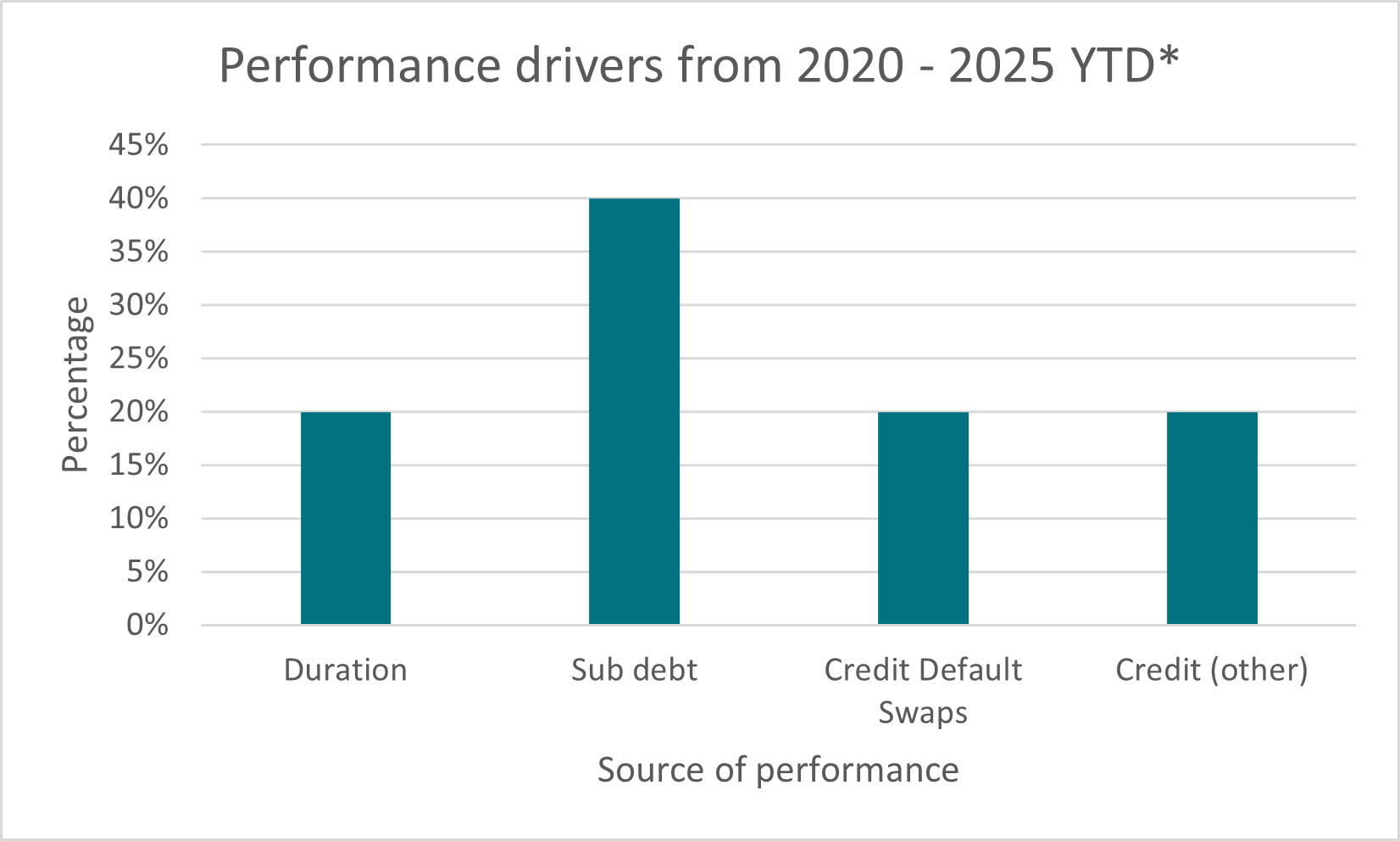

Conviction in High Beta Credit

One example of where taking a strategic allocation has been important is within high beta credit. Exposure to Financial Subordinated Debt and Corporate Hybrids has benefited from strong technical support, elevated carry, and improving issuer fundamentals. In 2025, spreads in high beta segments compressed meaningfully, reaching year-to-date tights. High Yield spreads tightened by over 150 basis points since April 2025, while yields remain attractive at approximately 5.1%2. Overall, we believe there is a compelling risk-return profile for Subordinated debt3 and selective allocation to High Yield.

If you look at the last five years, as demonstrated in the chart below, taking a selective positioning in this space has contributed significantly to performance. For such reasons, we maintain our conviction in the segment’s ability to navigate a complex macroeconomic landscape and deliver value.

Source: AXA IM, as of 30 September 2025 Performance drivers calculated from a Total Return strategy between 2020 and 2025 YTD. *YTD as of 30 September 2025. Past performance is not a reliable indicator of future results.

Building for the future

Despite growing uncertainty, driven by geopolitical tensions, trade disruptions, and fiscal policy ambiguity, Euro credit spreads remain close to historical tights, supported by resilient fundamentals and strong technicals.

One sector that we believe continues to stand out is the Banking sector. European banks have posted robust performance in 2025, with equity prices up over 55% year-to-date4, significantly outperforming broader indices. This strength is underpinned by solid capital positions, resilient loan demand, and stabilising net interest margins.

From a fixed income perspective, bank debt offers compelling value and some diversification away from the impact of US tariffs on global growth. Credit fundamentals remain sound, with low default risk, and strong capitalisation ratios well above the regulatory thresholds.

Investor appetite is growing, particularly for subordinated bank debt, as spreads remain attractive relative to other sectors. With banks increasingly focused on digital transformation and cost efficiency, the sector should be well-positioned to navigate structural shifts and deliver stable income to bondholders.

The benefit of flexibility

A sector’s influence on a portfolio’s performance will invariably depend on the macroeconomic conditions as well as market demand and credit availability. While issuer quality should be more important than sector allocation, being able to adapt to various market conditions and move across sectors to benefit from opportunities may be instrumental for adding value, especially during times of volatility.

In today’s landscape, marked by rising political risk, trade tensions, and policy uncertainty, we’ve adopted a more conservative risk stance than earlier in the year. The potential for disruptive tariff policies, geopolitical fragmentation, and uncoordinated monetary easing across major economies has increased market sensitivity.

Nonetheless, we believe European issuers’ credit quality is in good shape, enabling them to withstand a potential economic slowdown. If risk assets experience temporary dislocations, the combination of healthy corporate fundamentals and persistent investor inflows into euro credit should continue to offer attractive opportunities for long-term investors.

- Source: Bloomberg, as of 30 September 2025

- High beta credit are fixed income corporate securities that exhibit greater sensitivity to market movements, often providing higher potential returns but also increase risk.

- Source: https://stoxx.com/index/sx7e/

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.