Harnessing the power of duration in global bond portfolios

KEY POINTS

Following the rise of global interest rates on the back of much higher inflation over the last few years, investors are now focusing on the expectation for lower official rates, as the tightening of financial conditions has spurred on central banks to start loosening monetary policy.

Such a backdrop typically delivers a positive boost for bond returns, but what we are finding is the path to lower interest rates and lower bond yields is not that simple. As active top-down managers of global portfolios, we believe the power of duration and its impact on total returns should not be overlooked.

Managing duration is not just a question of owning duration, or not; in a global context there are different yield curves to be exposed to. It’s also possible to own ‘lots’ of duration, but to do that in the shorter part of the yield curve. So, we think about overall duration exposure, the geographic curves that we have exposure to, and finally which maturity part of that curve is likely to be the most impactful.

Different bond curves

Bond market yields reflect evolving expectations of global interest rates. In recent cycles, especially in a world of quantitative easing-manipulated yield curves, expectations surrounding global interest rates generally converged around the US. However, diverging fiscal policies and countries being at different points in their economic cycle means there are differences in the approaches of major central banks and, consequently, dispersion in both the direction and level of core government bond yields.

As top-down managers, this dispersion brings the opportunity to actively manage duration exposure across countries by taking exposures to different interest rate curves to reflect the varied growth and inflation prospects across the global economy.

Looking back over previous quarters, the chart below shows how the German and US bond yields, while often moving in the same direction can outperform or underperform each other. Typically, this is driven by a combination of factors, but certainly economic fundamentals and differing central bank polices play an important role.

In addition, bond market sentiment alongside supply and demand dynamics evolve and reflect differing outlooks. The relative movement across different curves can therefore create opportunities to enhance returns. This combination of diversification across different yield curves, alongside active fund management should enable investors to benefit from government bond markets.

Different maturities along the yield curve

In the same way that different yield curves evolve, the shape of the yield curve is in constant flux. As all-maturity bond investors, it is our job to analyse these changes and adjust portfolios to gain exposure to the parts of the curve that represent attractive opportunities and compliment the rest of the strategy.

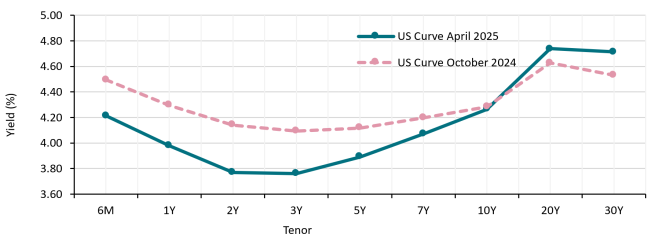

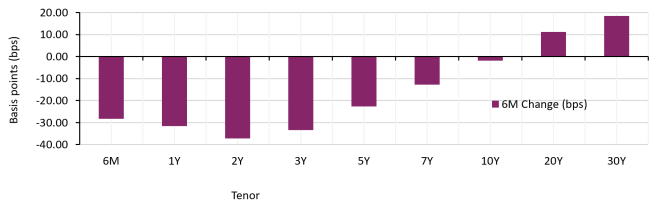

The current market trend is for bond curves to ‘steepen’ which means that shorter maturities are outperforming longer-dated maturities on the expectation that interest rates should get cut. Being the bond market however, there are various, sometimes complex ways, that this can manifest itself. A bullish steepening is where all yields move lower, but short-dated outperform their long-dated equivalent. A bearish steepening will see the same outperformance but where all yields rise. It is clearly also possible that short-dated bonds can move lower and longer-dated bonds can move higher.

A common misconception is that to build a bullish duration position, you need to own longer-dated bonds. To build the same outright duration risk but at the short end of the curve, you simply need to be exposed to more short-dated bonds.

To bring this to life, we can look at the steepening of the US Treasury yield curve over the past six months. The steepening has been driven by both falling front-end yields and rising long-end yields. Had a long duration position been built by exposure at the long end, the duration risk factor of the portfolio would have been a drag on returns; however, a long duration position through shorter-dated bonds would have boosted performance.

If you stop to look around, you just might miss it

Markets are moving quickly. Uncertainty around tariffs and their potential impact on inflation; rapid geopolitical developments; fiscal policy shifts; and a less than clear path for central banks all seem to be driving a period of rates volatility. Therefore, by harnessing the return power of duration, we believe investors should potentially benefit from both diverse and actively-managed duration exposure in bond portfolios.

We are constantly monitoring the macroeconomic environment to determine tactical duration positioning. In our global bond portfolios, cash bonds are an important source of duration risk, but using futures to manage duration risk provides even more flexibility. We describe the use of futures as our duration overlay, allowing portfolio managers to rapidly and dynamically implement duration views in anticipation of market events, or as they unfold. To reflect these views, we buy or sell government bond futures in a specific currency and maturity. By taking this approach we seek to add, cut, neutralise, or tweak our duration exposure and target these views across regions or maturities, or both.

In conclusion, we’re in a new era marked by higher rates volatility and wider dispersion in yields across core government bond markets. This environment offers more opportunities for managers who can adopt a dynamic, flexible, and tactical approach to duration risk, thereby unlocking the true potential of one of fixed income's major performance drivers.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.