How to generate performance in a credit portfolio

KEY POINTS

It has already been a tale of two cycles this year with the positive sentiment and stable growth experienced at the start of 2025 tumbling into inflationary and recessionary concerns. Trade tensions have been a dominant theme in recent weeks and are expected to persist in the coming months. In such an environment, looking for ways to create returns while mitigating risks are paramount for investors.

Fixed income is therefore a strong contender. Within this asset class, credit could be an attractive option as many companies have entered this unsteady period with strong balance sheets and sound fundamentals overall. Alongside this, absolute yields are still above levels seen for much of the past decade, maintaining some appeal. In Europe, credit should also benefit from falling rates, falling inflation and, albeit slow, growth. Overall, we think there are strong reasons to consider credit within a portfolio.

Generating performance from credit, particularly in challenging markets, isn’t always straightforward. Fortunately, there are many levers to pull especially if taking a flexible approach that aims to identify sources of value, take advantage of market anomalies, and adapt to market fluctuations.

We use a robust investment process to select issuers across sectors, regions and credit ratings. The process is important as issuer selection can improve or detract from the overall performance. Alongside return considerations, the allocation across these different factors helps provide diversification, mitigate credit risk and reflect best ideas within a portfolio.

Sector allocation

Different sectors will respond differently to market conditions. Typically, when economies are slowing or during times of stress, we expect defensive sectors (eg utilities and telecoms) to perform better than cyclical sectors (eg automotives and capital goods) as they are less likely to be impacted by an economic slowdown. For example, the market’s response to the US tariffs was one of heightened risk aversion. In this environment, defensive sectors were more resilient, showing smaller moves compared to the greater volatility seen in cyclical sectors.

Credit allocation

Credit ratings indicate the likelihood of an issuer defaulting on its payments. If a bond is investment grade, it will have a high credit quality rating because it is considered less likely to default on its payments and, therefore, seen as less risky. High yield bonds, on the other hand, have a lower credit rating but tend to offer higher income in return.

Creating the right balance between investment grade for credit risk mitigation and high yield for enhanced income returns can be a strong performance driver. Our total return strategy, for example, maintains flexibility across credit market, with a historical average allocation to high yield of around 30% since inception

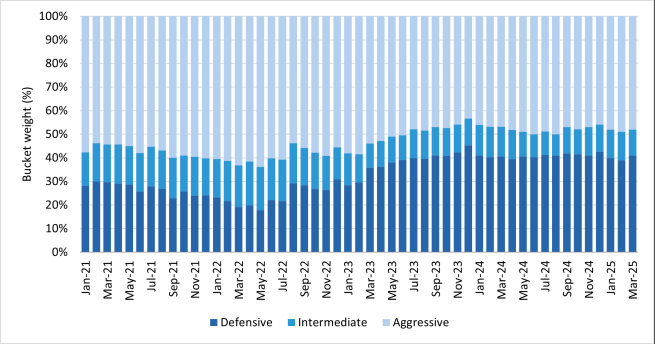

In order get the most from our asset allocation, we divide the investment universe into three risk categories defined according to the fundamentals and characteristics of the markets in which we invest.

- Defensive: This includes cash equivalent and very high-quality corporate bonds from core European countries such as France and Germany. This risk bucket is generally quite defensive and offers low volatility and high liquidity characteristics

- Intermediate: Corporate bonds that are still highly rated but in European countries considered periphery such as Italy and Spain. This bucket should provide more yield opportunities and a little more volatility

- Aggressive: High yield and subordinated bonds across the different geographic regions which should provide high levels of yield but also increase the amount of volatility

By investing flexibly and dynamically in these three pockets of risk depending on the market environment, we aim to generate solid risk-adjusted returns.

Duration

Interest rate risk is an important consideration in bond portfolios. Short duration bonds – typically bonds with one-to-three years maturity – are less sensitive to interest rate changes than bonds with longer maturities. This is because long duration bonds which often have maturities of 10 years or more, are more vulnerable to interest rate changes due to the uncertainty of future economic conditions and interest rate environments.

The ability to manage duration allows us to adjust the portfolio’s interest rate sensitivity, aligning it with both current market conditions and longer-term trends. For instance, in a declining rate environment, we can aim to capitalise on price appreciation by increasing exposure to long-duration bonds. Conversely, in a rising rate environment, we should be able to mitigate potential losses by favouring short-duration bonds. This strategic flexibility gives us the opportunities to optimise portfolio performance while seeking to provide valuable downside protection in periods of interest rate volatility.

Volatility has the final word

The word volatility can bring dread to an investor’s heart as it suggests slumps in returns. However, what is often overlooked is that volatility can also offer opportunities. We welcome volatility, as it allows us to implement our views much more dynamically than in a sluggish market. A flexible management approach should enable us to capitalise on market overreaction, buying when others may be selling in panic. In this way, we see volatility not as a risk, but as an opportunity to enhance returns.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.