In medias res

With updates on the Middle East conflict coming minute by minute, one can only observe the market’s reaction to the latest developments, attempt to divine the implicit assumptions, and imagine scenarios for how the situation might evolve.

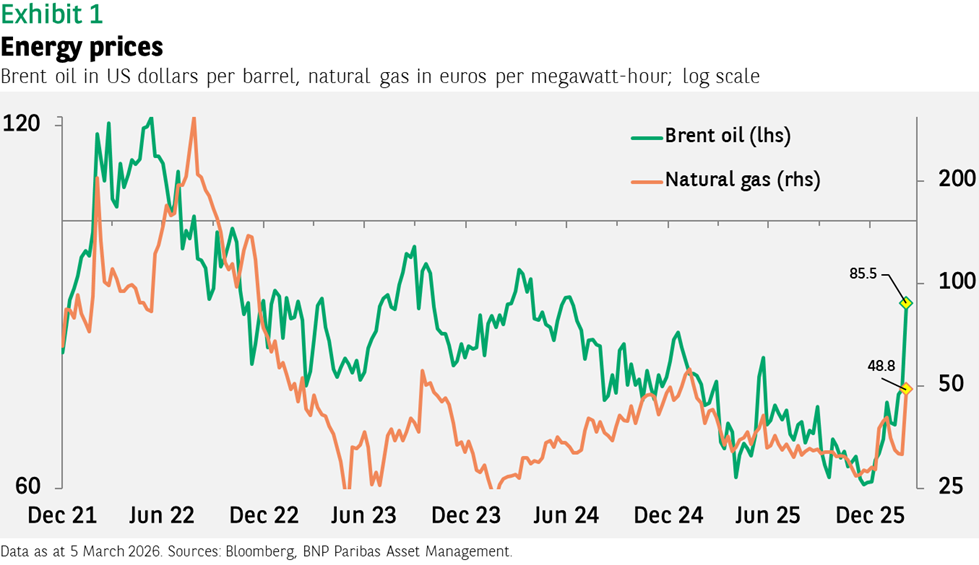

The single most important market price in our view is that of Brent crude oil. At the time of writing, Brent oil was trading at $86 per barrel, a 20% increase from the previous Friday’s close (see Exhibit 1). While a meaningful increase, it is less than the worst predictions of $100-plus and below previous peaks of the last few years. Market expectations point to a decline in the weeks ahead. The implicit market view of the progress of the war, then, seems to be that it will continue for weeks, not months, and the conflict’s intensity will decrease over time. The reported drop in the number of missiles and drones launched by Iran over the last few days supports this view. A total block of traffic through the Strait of Hormuz should be avoided (Iran also needs to be able to export its own oil, so it is not in the country’s interests to close the passageway). These assumptions could clearly change at any moment if, for example, a critical energy node is struck.

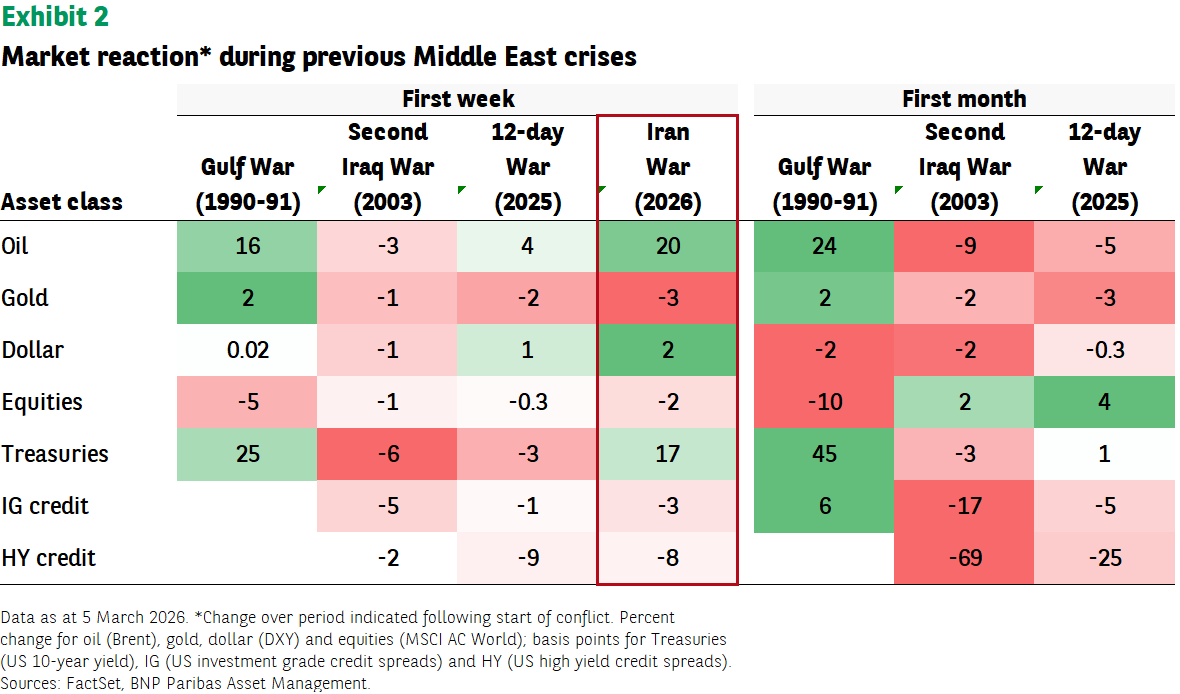

Other asset classes have generally performed as one would expect (this is not the first crisis in the Middle East), though there is still variation compared to previous episodes. Oil prices have gained more than they did during the Gulf War, and the US dollar has strengthened more than it did during the other crises, belying somewhat the “sell America” mantra (see Exhibit 2).

US Treasury yields have risen over the last week as inflation worries offset the asset’s perceived ‘safe haven’ appeal. The decline in equities has been moderate, but this obscures a wide range of returns across different industries: precious metals have dropped 16% and airlines 9% while oil stocks are up 4%-5%.

The crisis has triggered a reversal of some previously successful (or unsuccessful) trades as extreme long or short positions get washed out. For example, the MSCI Korea index, which had surged 58% in local currency terms year to date, has fallen 12% since Friday 27 February. Japanese equities have suffered similarly. US software stocks, by contrast, have rebounded after their notable underperformance of the last several months, gaining 4% over the week.

As with any crisis, asset prices change, which may lead to opportunities (at the appropriate time) to establish positions at more attractive valuations. Despite the turmoil provoked by the war, it has not (yet) changed our fundamentally constructive outlook for risks assets this year. For that to happen, we would need to see oil prices rise much more and then stay at an elevated level for an extended period of time.

And elsewhere …

While the war understandably dominates headlines and investors’ attention, economic data continues to be released, providing us with an ongoing assessment of the health of the global economy. The caveat is that these figures do not reflect the current situation, but they nonetheless give us a picture of how weak or strong economies are in the face of the new challenges.

The picture over the last week has been encouraging. The expansion in business activity, as measured by Purchasing Managers’ Indices, looks to be continuing in the services sector. The US stands out as the February ISM Services index jumped to 56.1, the highest level in four years (a reading above 50 indicates expansion). For the manufacturing sector, the figures are more modest, mostly just above 50, but those for the largest European countries are all above 50 for the first time in many years.

The surprisingly weak US non-farm payrolls figure, alongside negative revisions to the prior month, will assuage worries about an overheating economy. This may offset some of the inflation worries stemming from the rise in oil prices and bolster support for cuts from the US Federal Reserve this year.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.