Take Two: Global stocks endure fresh volatility; Eurozone inflation falls

What do you need to know?

Global stocks endured a fresh bout of volatility last week amid renewed uncertainty over US trade policy but were subsequently boosted by strong corporate earnings. The MSCI World NR Index rose 1% over the week to Thursday’s close*, while the UK’s FTSE 100, Euro Stoxx 600 and Japan’s Nikkei reached fresh record highs. Markets fell at the start of last week following US President Donald Trump’s announcement of fresh tariffs, after the US Supreme Court overruled some of the levies imposed in 2025. Global indices then recovered as the new tariffs came into effect at a lower rate than initially expected.

* In US dollar terms. Source: FactSet, data as of 26 February 2026

Around the world

Eurozone annual inflation fell to 1.7% in January, in line with the preliminary estimate and down from December’s 2.0%. The 16-month low reflected a fall in energy prices and a slowdown in services inflation. Core inflation, which excludes energy, food, alcohol and tobacco, edged down to 2.2% from 2.3%. Separately, Germany’s economy returned to growth in the fourth quarter of 2025, expanding by 0.3% on a quarterly basis after a flat reading in Q3. The rise was primarily driven by household and government spending.

Figure in focus: RMB 803.5 billion

Tourism spending in China reached a record RMB 803.5 billion (around US$117 billion), from some 596 million domestic trips taken during the Lunar New Year holiday in February. Both figures represent an almost 19% increase from the same period last year, according to Reuters. This year’s Spring Festival was extended from eight to nine days, in a government effort to boost consumer spending and encourage households to travel, shop and seek entertainment. However, spending per domestic trip fell slightly by 0.2%. The slight dip could suggest Chinese consumers remain cautious despite government stimulus.

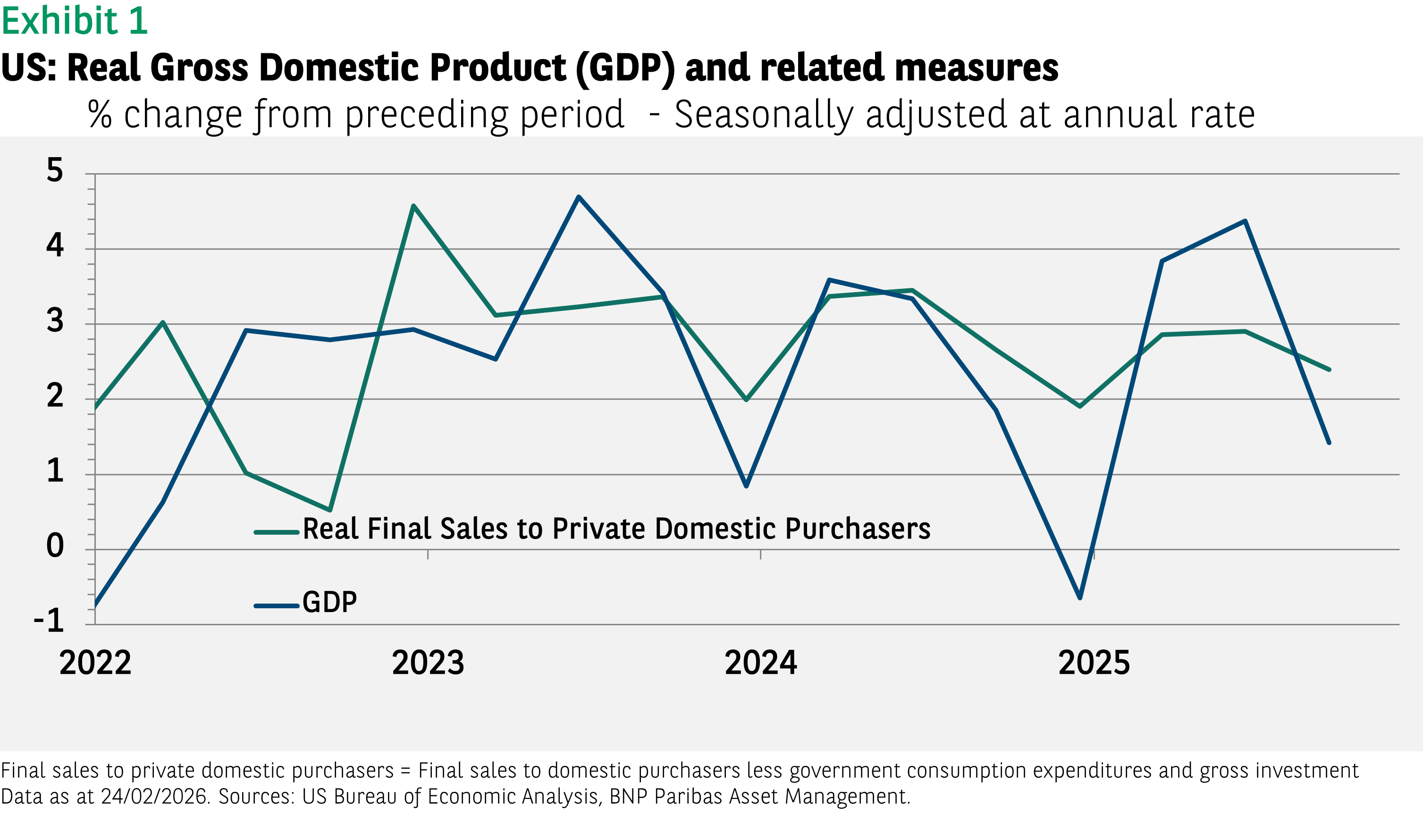

Chart of the week

Fourth quarter US GDP growth came in at 1.4% (seasonally adjusted annual rate), the recent advance estimate showed. It was both a slowdown from Q3’s 4.4% and disappointing versus consensus estimates. Nevertheless, the underlying data was more encouraging. First, there was a sizeable drag to quarterly GDP growth (-0.9 percentage points) from lower federal government consumption and spending, because of the partial government shutdown. Second, final sales to private domestic purchasers have been much less volatile than GDP. Private domestic demand (consumption plus investment) has been hovering around 2.5% for the past two years, underlining US growth’s resilience.

Words of wisdom

HALO Trade: Companies with tangible assets and a lower risk of disruption from technological change have garnered investor and media attention recently, amid concerns over artificial intelligence spending and threats to company business models. Those with heavy assets and low obsolescence – the so-called HALO trade – include companies in the commodities, infrastructure, logistics, and food sectors, among others. These are generally viewed as defensive sectors that could prove more resilient in periods of macroeconomic uncertainty. While technology and AI could potentially improve efficiency and productivity in such areas, the underlying assets themselves are unlikely to be replaced.

What’s coming up?

On Tuesday, the Eurozone issues a preliminary estimate of February’s inflation rate, and the UK government delivers its Spring Statement where it will outline its growth and spending expectations. Wednesday sees several final composite Purchasing Managers’ Indices released, including those covering Japan, China, the Eurozone, US and UK. China’s Two Sessions, its annual legislature and policy meetings, begin on Wednesday and will see the government announce its next five-year plan for economic growth. On Friday the Eurozone publishes the final estimate of its Q4 GDP growth rate, and the US updates the market with jobs data.

Read more insights at the Investment Institute

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.