How to integrate Green Bonds in a Global Allocation

- 26 September 2023 (3 min read)

Key points:

- Green bonds remain one of the most appropriate instrument to deliver environmental benefit while gaining access to a global, diversified and well-balanced universe

- Investors’ appetite remains strong for the asset class, but they can face a tracking error dilemma

- Green bonds combined with a small allocation to US Treasuries potentially offers the benefits of investing in green bonds while addressing the tracking error dilemma

Growth of the Green bond market and opportunities

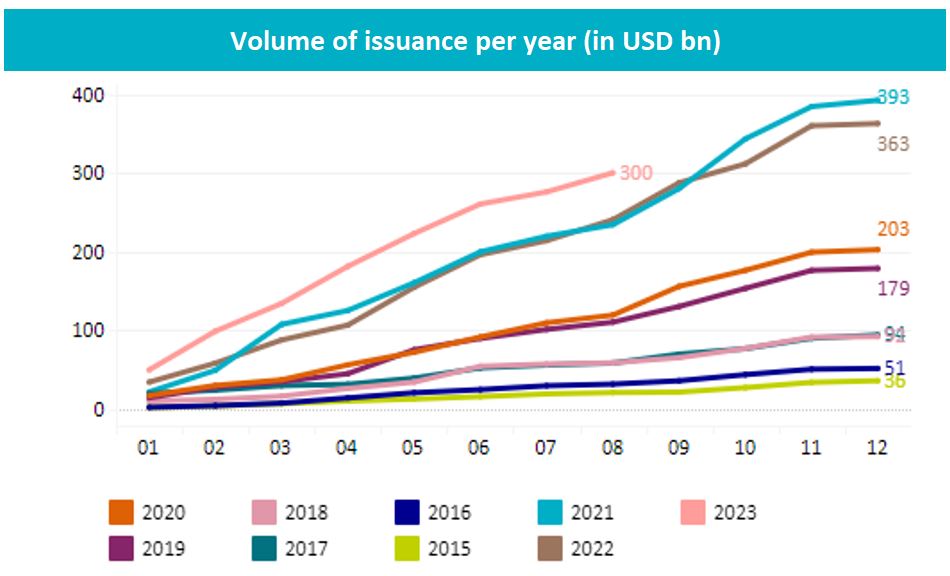

Over the past few years, the green bond market has grown from a niche market to a credible alternative to the conventional bond market. So far this year, green bonds issuance is up 25% of the previous record levels reached in 2022 and 20211 thanks to continued credit sector diversification and increasing sovereign issuances. Historically, investors have been attracted to the asset class due to the benefit of higher transparency, the ability to track the projects financed, assess their environmental benefit, and measure it with clear KPIs. Now, this trend of strong issuance levels allows green bonds to offer investors a global and diversified universe worth more than $1.4trn with more than 700 issuers.

Source: AXA IM, Bloomberg as of 31 August 2023

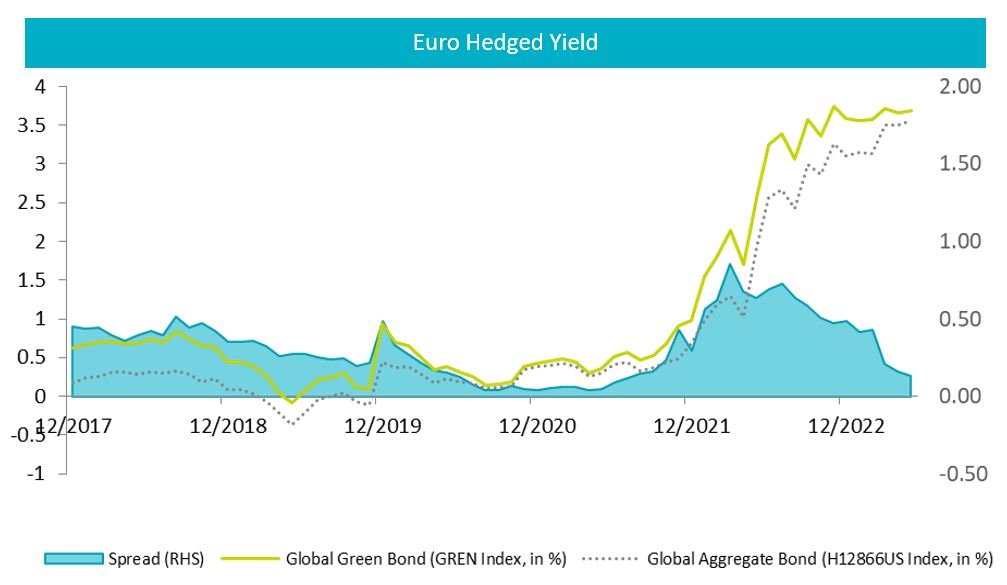

Strong investors’ appetite

Institutional investors were the first to grasp the potential of the instrument in a context of growing awareness around climate change risks, increased demand for transparency and regulatory scrutiny. Yet, it did not take long for wholesale and retail investors to be won over by green bonds as well in a rush for credible sustainable investment solutions. As rates hit multi-year highs, green bonds now also offer the possibility to capture attractive yields levels and a decent pick-up compared to the conventional universe, at a moment when central banks are reaching their peak rates.

Source: AXA IM, Bloomberg as of 31 August 2023

Yet, if some investors have the flexibility to build a custom allocation in which green bonds fit perfectly, many still run strategic asset allocations based on conventional benchmarks and face a tracking error dilemma.

The tracking error dilemma

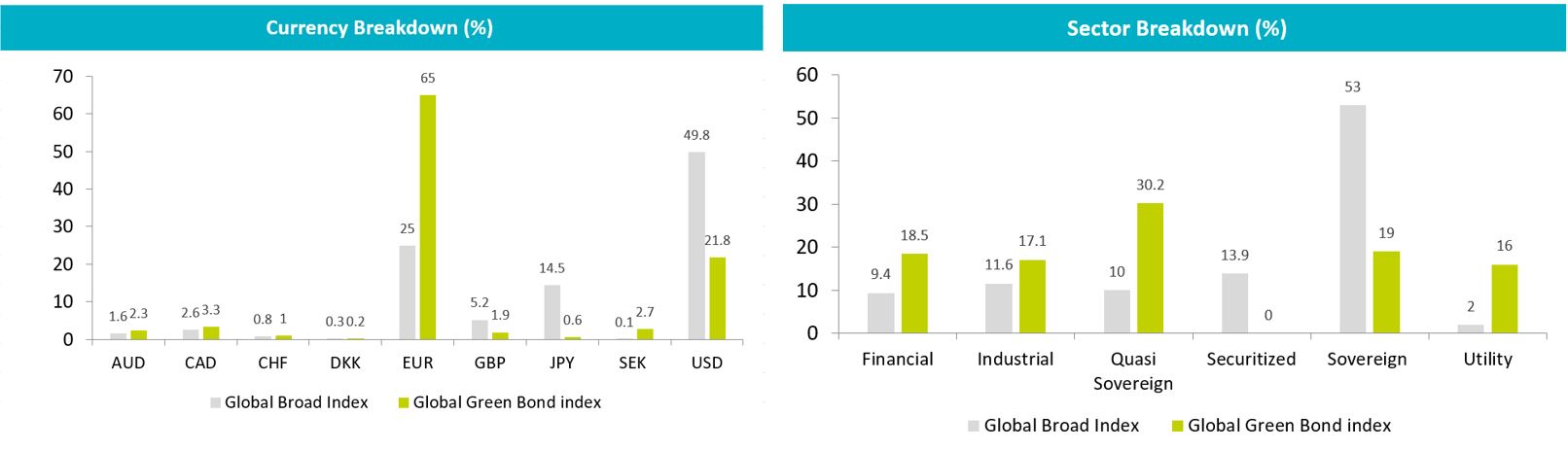

While the green bond market may have converged towards the conventional bond market when it comes to average duration or ratings, some differences remain. The green bond universe is more concentrated towards euro and dollar currencies and offers higher exposure to credit debts than the conventional market.

Source: AXA IM, Bloomberg as of 31 August 2023

These differences imply a close to 200bps tracking error between a global green bond and a global aggregate index. This did not translate historically into major performance differences with a correlation between the two universes over the past five-year standing at around 91%2 . Yet, the rebound in rates volatility seen in 2022 has highlighted that these differences should not be ignored when considering a green bond allocation against a conventional aggregate benchmark.

Combining green bonds with US treasuries

We believe there is a very simple way to allocate to green bonds while addressing this dilemma. We found that combining green bonds with US Treasuries should increase the performance correlation and decrease the tracking-error against a global aggregate universe. This combination addresses the two key differences we highlighted between green bonds and the conventional market with a very liquid and low-cost approach.

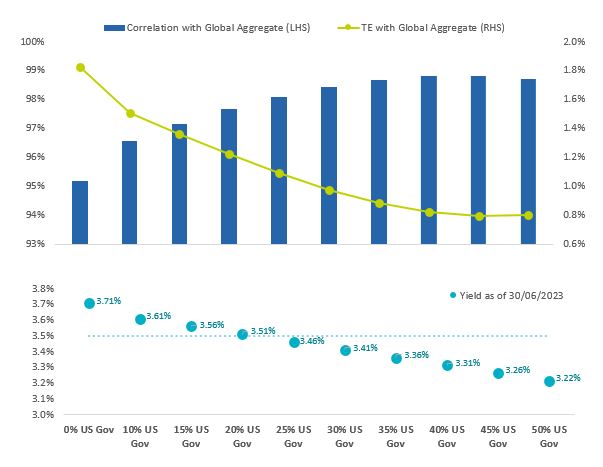

In order to define the most optimal allocation, we ran a series of portfolios combining green bonds with up to 40% US Treasuries. The results demonstrated that with up to 25% allocation to US Treasuries, tracking error should decline and performance correlation improve while maintaining a higher, or similar, yield level. Yet, when continuing to allocate more to US treasuries, it is likely the correlation will hit a cap before declining, and tracking error hits a floor.

Source: AXA IM, Bloomberg as of 31 August 2023

We believe that a 75% allocation to green bonds combined with 25% US treasuries would be a potentially optimal way to gain exposure to green bonds, minimise tracking error, maximise correlation and preserve the yield of the resulting allocation. Indeed, such combinations should offer a 98% correlation with a global aggregate universe (up from 91% for green bonds alone) with 1% tracking error (half of what the green bond universe exhibited).

Looking forward

The green bond market has become increasingly dynamic and should continue to offer interesting investment opportunities going forward. The benefit of transparency, the measurability, competitive yields both in absolute and relative terms make this well-balanced universe particularly attractive for investors looking for attractive valuations and a credible sustainable solution. Whether they opt for a custom approach to the green bond universe or a combination strategy, we believe investors can take advantage of the universe with approaches that are innovative and yet straightforward.

- U291cmNlOiBBWEEgSU0sIEJsb29tYmVyZyBhcyBvZiAzMSBBdWd1c3QgMjAyMy4gSXNzdWFuY2UgbGV2ZWxzIHJlYWNoZWQgJDMwMGJu

- U291cmNlOiBBWEEgSU0gYXMgb2YgMzFzdCBKdWx5IDIwMjM=

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.