Take Two: Fed’s inflation concerns keep rates on hold; Japan returns to growth

What do you need to know?

US interest rates could remain on hold “for some time”, due to persistent inflation concerns, according to the Federal Reserve’s latest policy meeting minutes. The Fed, which kept its benchmark rate on hold at a range of 3.5%-3.75% in January, cautioned that progress towards its 2% inflation target might be “slower and more uneven than generally expected” and cuts may not be justified until “there was clear indication that the progress of disinflation was firmly back on track”. The US’s annual inflation rate eased to 2.4% in January, its lowest level since May.

Around the world

Japan’s economy returned to growth in the fourth quarter of 2025, expanding by 0.2% on an annualised basis, and recovering from Q3’s 2.6% contraction. However, the growth was considerably less than the 1.6% gain the market had been expecting. Meanwhile, Japan’s headline inflation rate fell to 1.5% in January from 2.1% the month before – coming in below the Bank of Japan’s 2% target for the first time since March 2022. Separately, Japan’s flash composite Purchasing Managers’ Index for February rose to 53.8 from 53.1, marking the private sector’s fastest rate of expansion since May 2023.

Figure in focus: €17 billion

The value of cross-border mergers between European Union banks rose to €17 billion last year - a post-global financial crisis record, according to the Financial Times citing Dealogic data. That compared to €3.4 billion in 2024 and was the highest since 2008’s €19.5 billion. The deals reflected rising profits and share prices as European banks build scale in a bid to take on larger US competitors. Worldwide, banking merger and acquisition activity rose by 129% to $190 billion in 2025, a separate report from consultancy McKinsey showed, while total financial services M&A rose by around 40% to $499 billion.

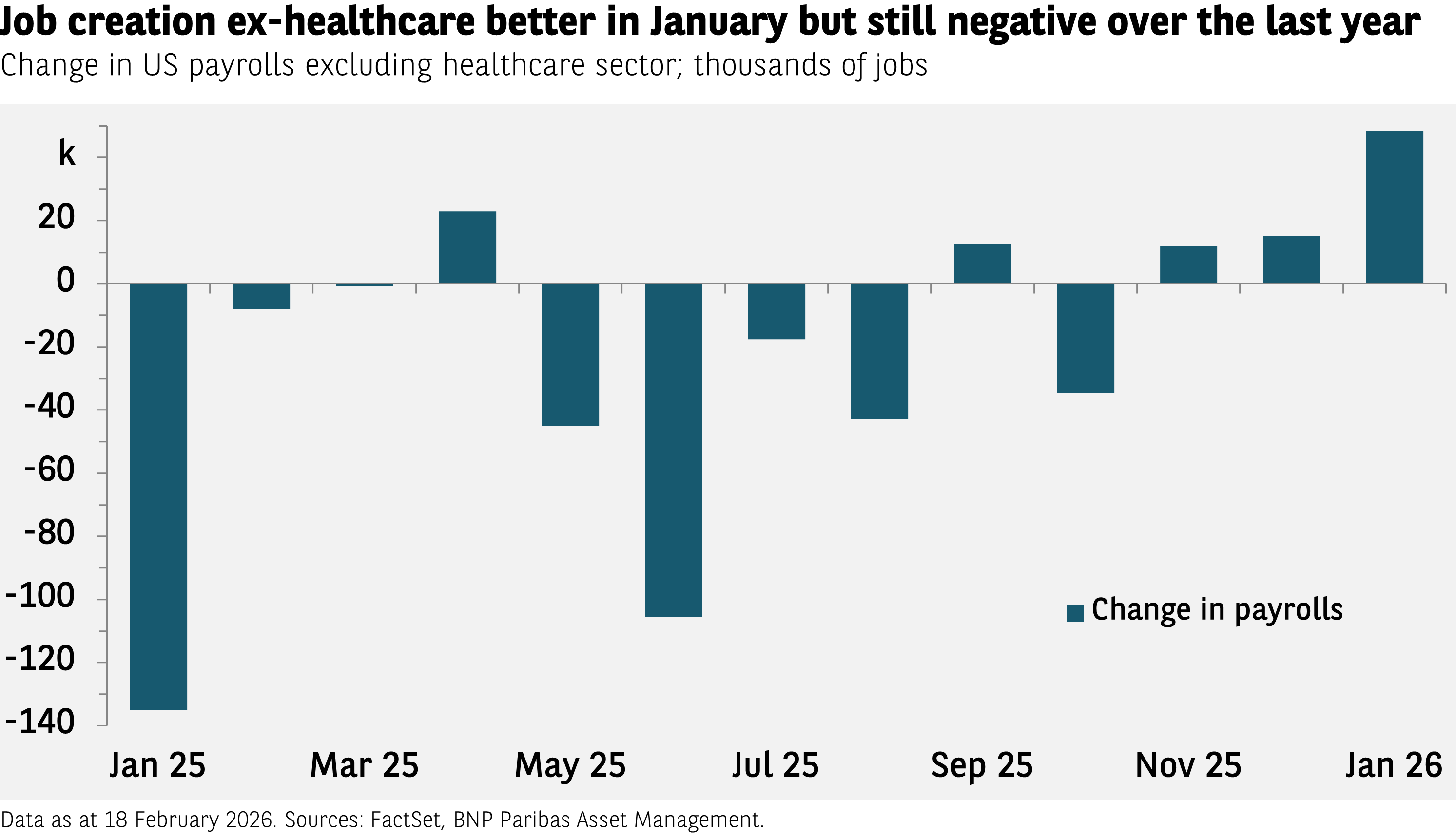

Chart of the week

Recent labour market data assuaged worries about US job creation. Excluding the healthcare sector (where job growth has been strong for years), 49,000 new posts were created in January. That still leaves the total for the last year, however, in negative territory. Some investors see the job losses as indicating a weak US economy. In fact, in our view, it is a sign of strength. GDP is rising, but the output is being generated with less labour – meaning productivity is going up. Where are the laid off workers going? Many are setting up shop on their own. We estimate about 800,000 sole proprietorships were established over the last year.

Words of wisdom: AI Impact Summit

India’s AI Impact Summit, which took place last week, brought together leaders from across the globe. The meeting’s aims included boosting global artificial intelligence cooperation and ensuring that technological developments and opportunities are shared more equally around the world. At the event, United Nations Secretary-General António Guterres called for a global $3 billion fund to build AI capacity in developing countries. Elsewhere, in a speech published last week, China’s President Xi Jinping emphasised the importance of accelerating AI development, to boost productivity and long-term economic growth. China’s so-called ‘AI-Plus’ strategy aims to integrate AI across key sectors including manufacturing, consumption, healthcare, education and agriculture.

What’s coming up?

On Monday Germany’s closely watched Ifo Business Climate indicator is published. Wednesday sees a final estimate of Germany’s Q4 GDP growth issued while the Eurozone reports its final estimate for January’s inflation rate. The previous report put inflation at 1.7%, down from 2.0% in December. On Thursday, a series of Eurozone surveys are published, including the bloc’s Economic and Industrial Sentiment measures. On Friday, the US issues its producer price index measure of inflation and Canada publishes its Q4 GDP growth rate.

Read more insights at the Investment Institute

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.